CASE STUDY 003 · EPLAN SERVICES

Real money, decided in a cluttered window.

ePlan's 401(k) tool asked people to rebalance portfolios, set allocations, and swap funds inside an interface that buried the very things they needed to see. I redesigned the whole experience — for first-time savers and spreadsheet-wielding accountants alike — and the error rate fell by more than half.

OUTCOME — errors −60% · support requests −29%

- Product Designer & Researcher

- Me · 1 PM · 1 product owner

- Spring 2021

- 401(k) experience, responsive web

- Audit · research · hi-fi · handoff

THE PROBLEM

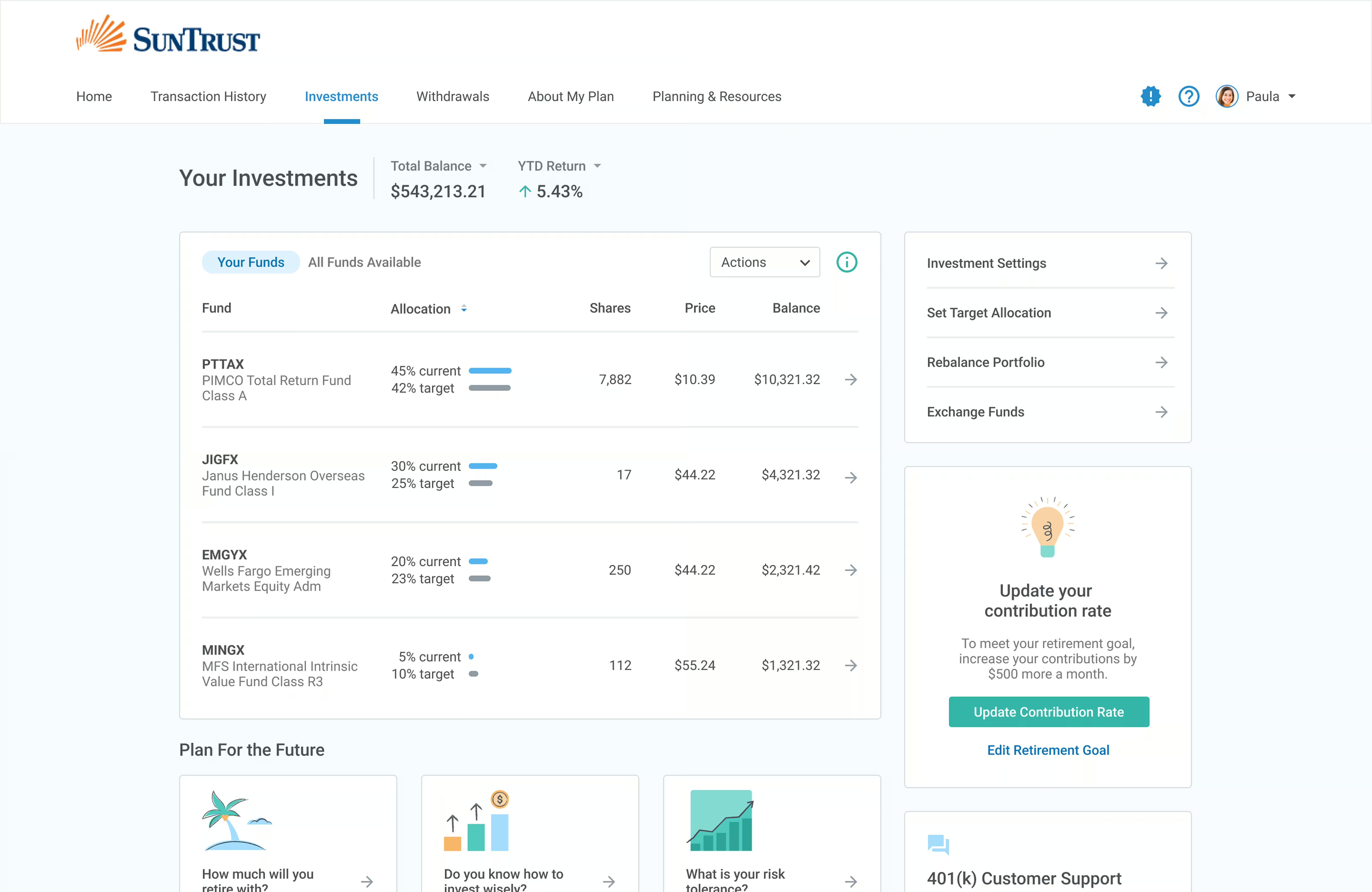

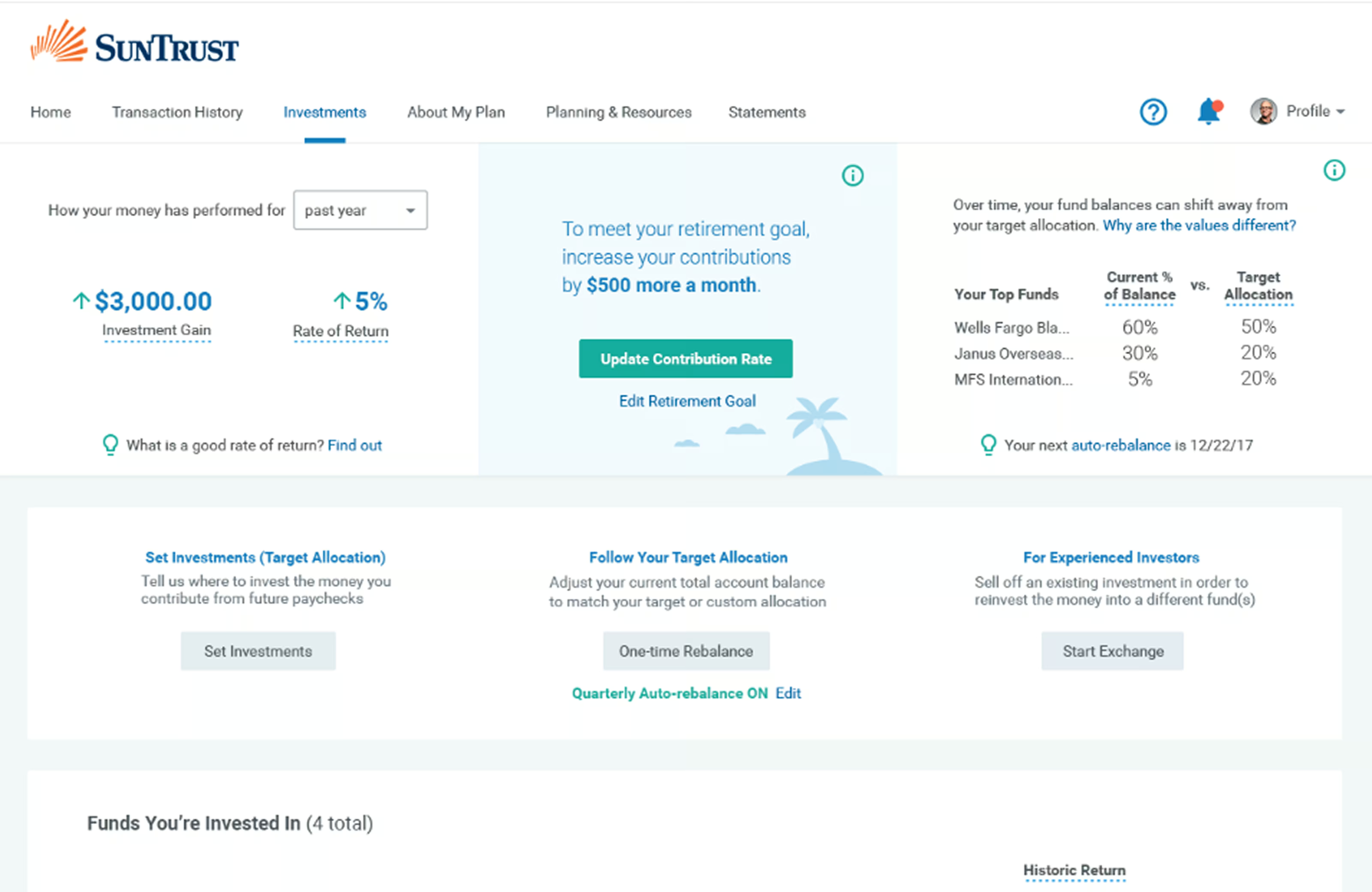

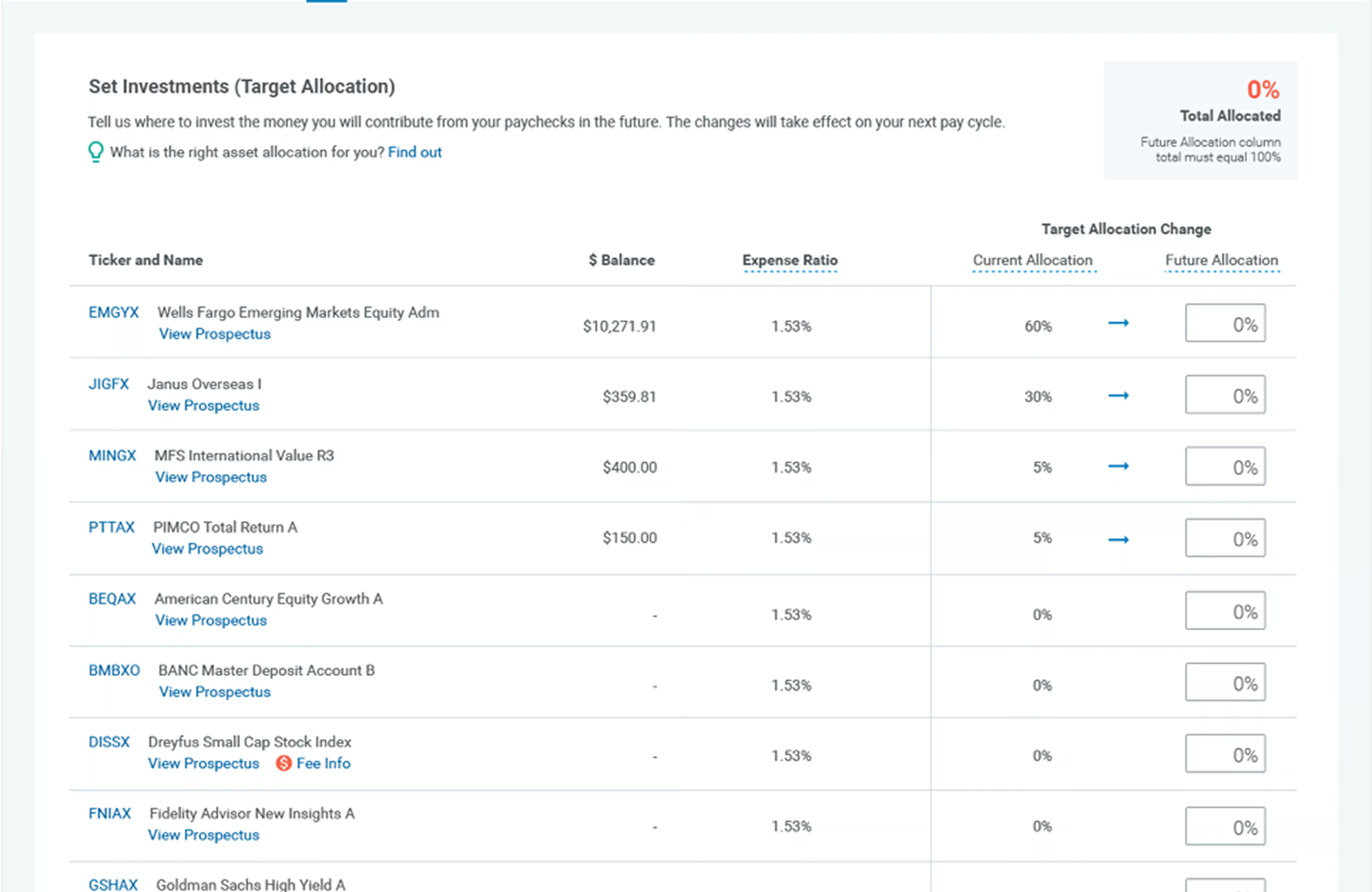

The product wasn't broken. Reading it was.

ePlan Services runs 401(k) plans, and the business problem stated itself: the investment tool was generating confusion, mistakes, and a steady drip of support tickets. Nothing was failing technically — balances were right, funds were all there. It was failing at legibility. Retirement investing is hard enough on its own; the interface was stacking friction in front of every consequential move.

I ran an audit before touching a single screen, and the trouble sorted into four problems that kept feeding each other.

WHAT THE AUDIT TURNED UP

- 01

Information overload — dense screens with no hierarchy to chunk them down.

- 02

No scaffolding for less-confident investors — the product assumed you already spoke the language.

- 03

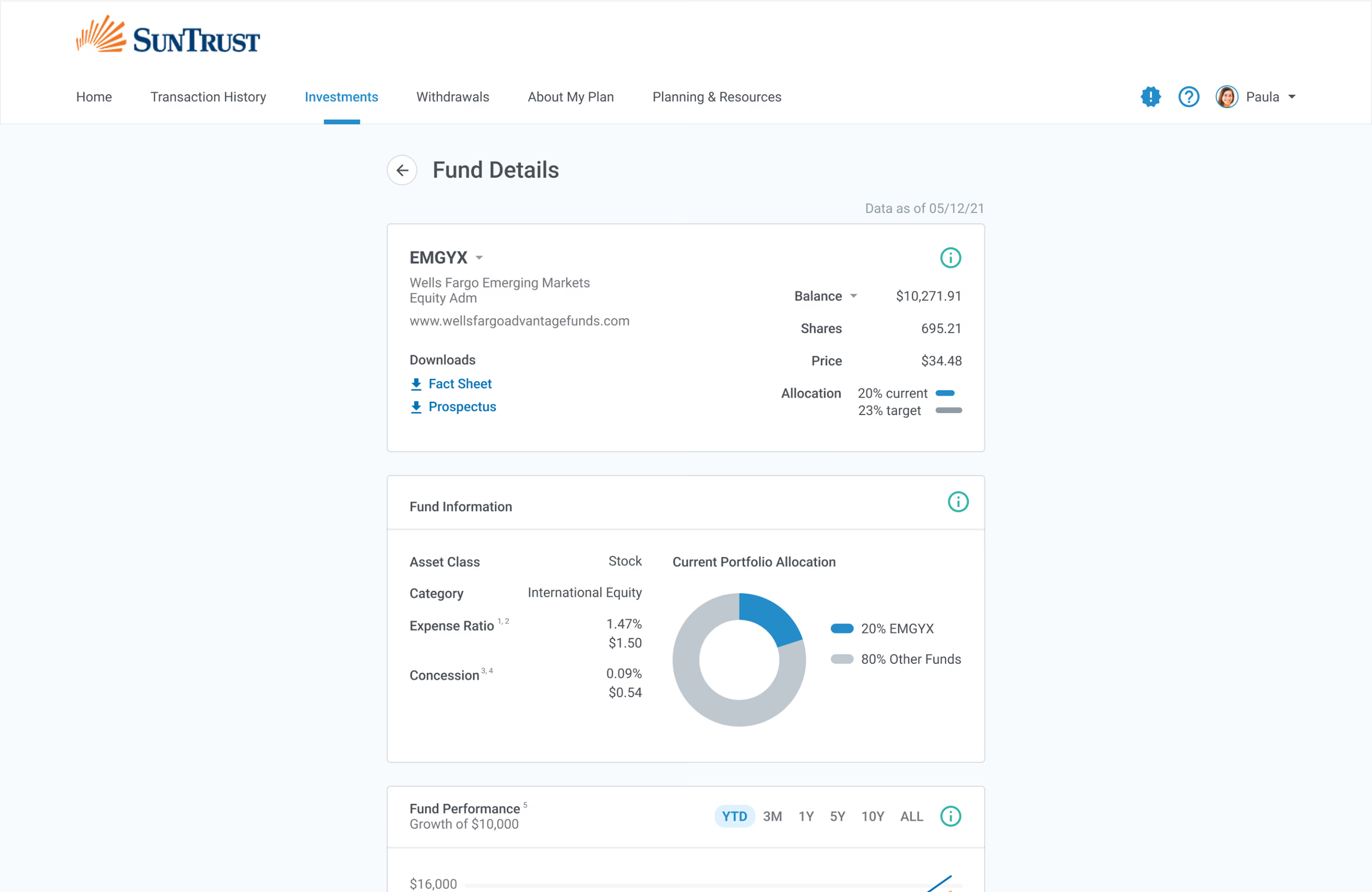

Data visualizations too thin to decide on — so people left the product to compare funds.

- 04

Inconsistent patterns flow to flow — every screen made you re-learn it.

WHERE IT STARTED /

WHERE I STARTED

I wrote down what I believed, then went looking for where I was wrong.

Instead of redesigning on instinct, I committed to three hypotheses before any design work started — partly to point the work somewhere, partly so the usability test had something concrete to confirm or kill.

- H1

Financial efficacy. Put literacy tools inside the product and people make better retirement decisions.

- H2

Error reduction. Make the management flows simpler and more sequential and people make fewer mistakes on the high-stakes ones.

- H3

Informed decisions. Surface the key comparisons clearly and people stop leaving the product to feel confident.

Generative research made the range of users impossible to ignore. The same product served a small-business owner who deferred to an advisor, an employee on a tight budget touching investments for the first time, and an accountant auditing the portfolio every month.

Designing for the median would have failed all three, so I didn’t. That spread is what drove the structural calls later — the IA had to flex across literacy levels without splitting into separate products, and the dangerous actions had to be hard to trigger by accident.

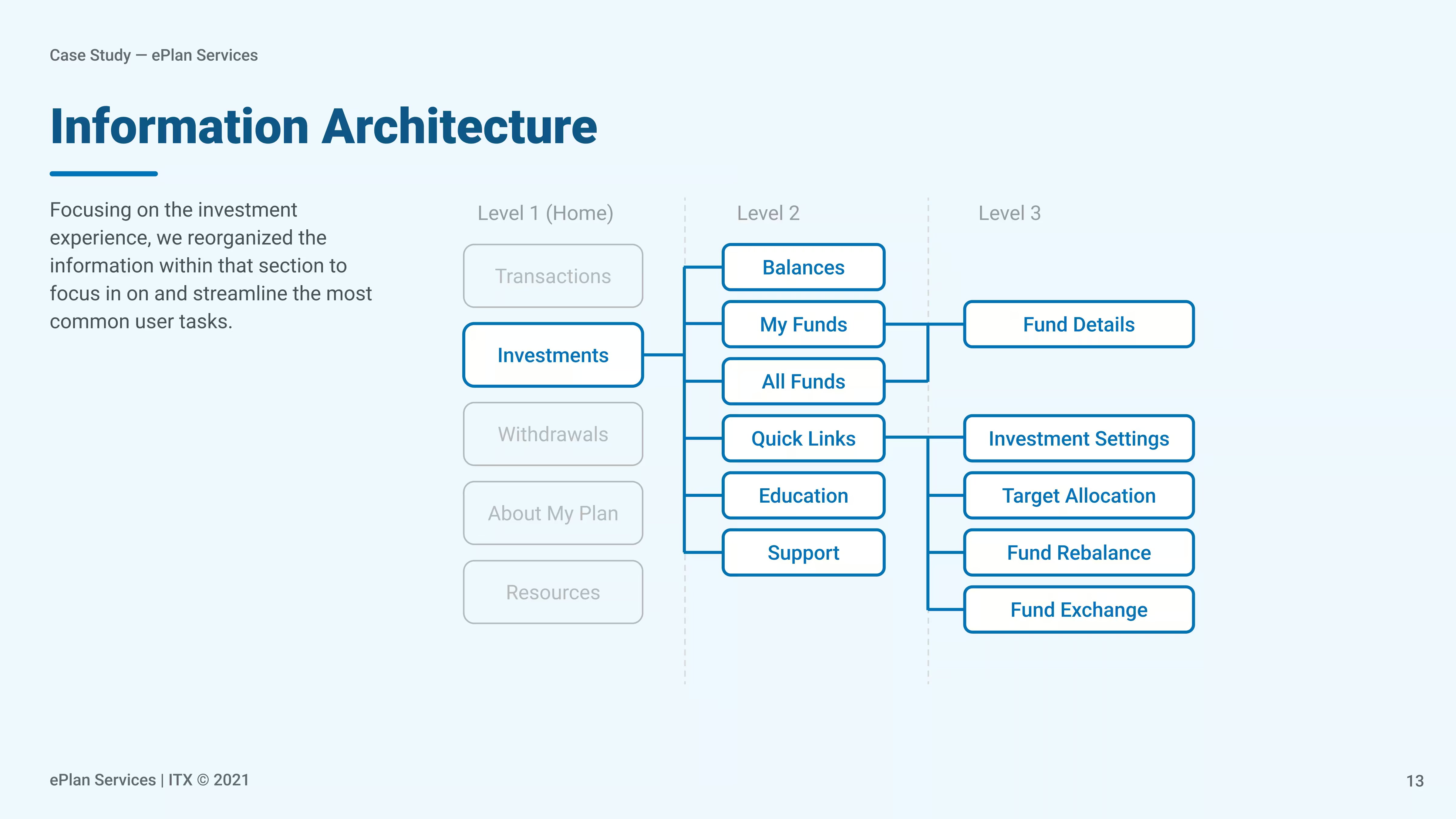

THE STRUCTURE

The fix was mostly structural: stop mixing looking with doing.

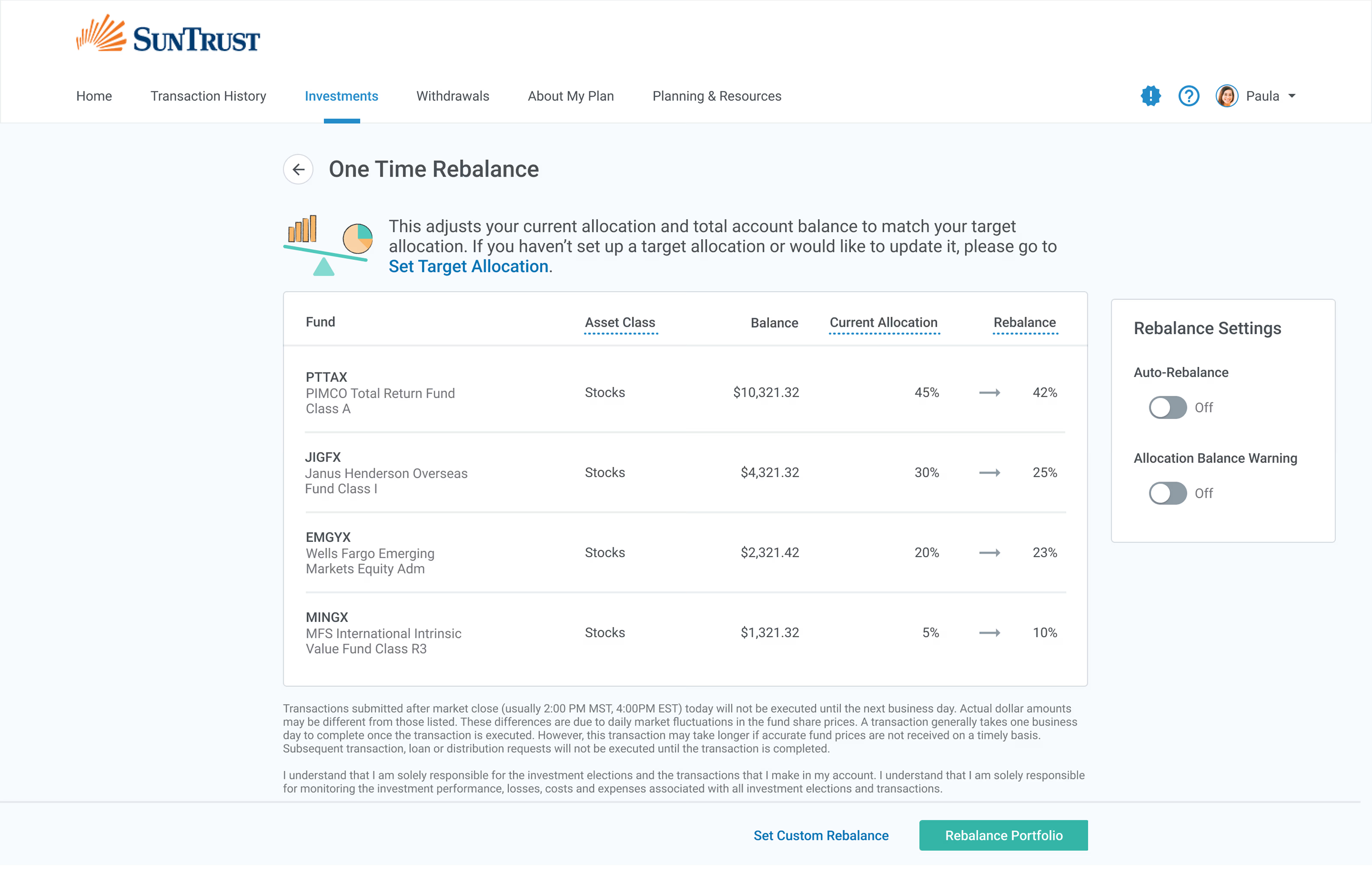

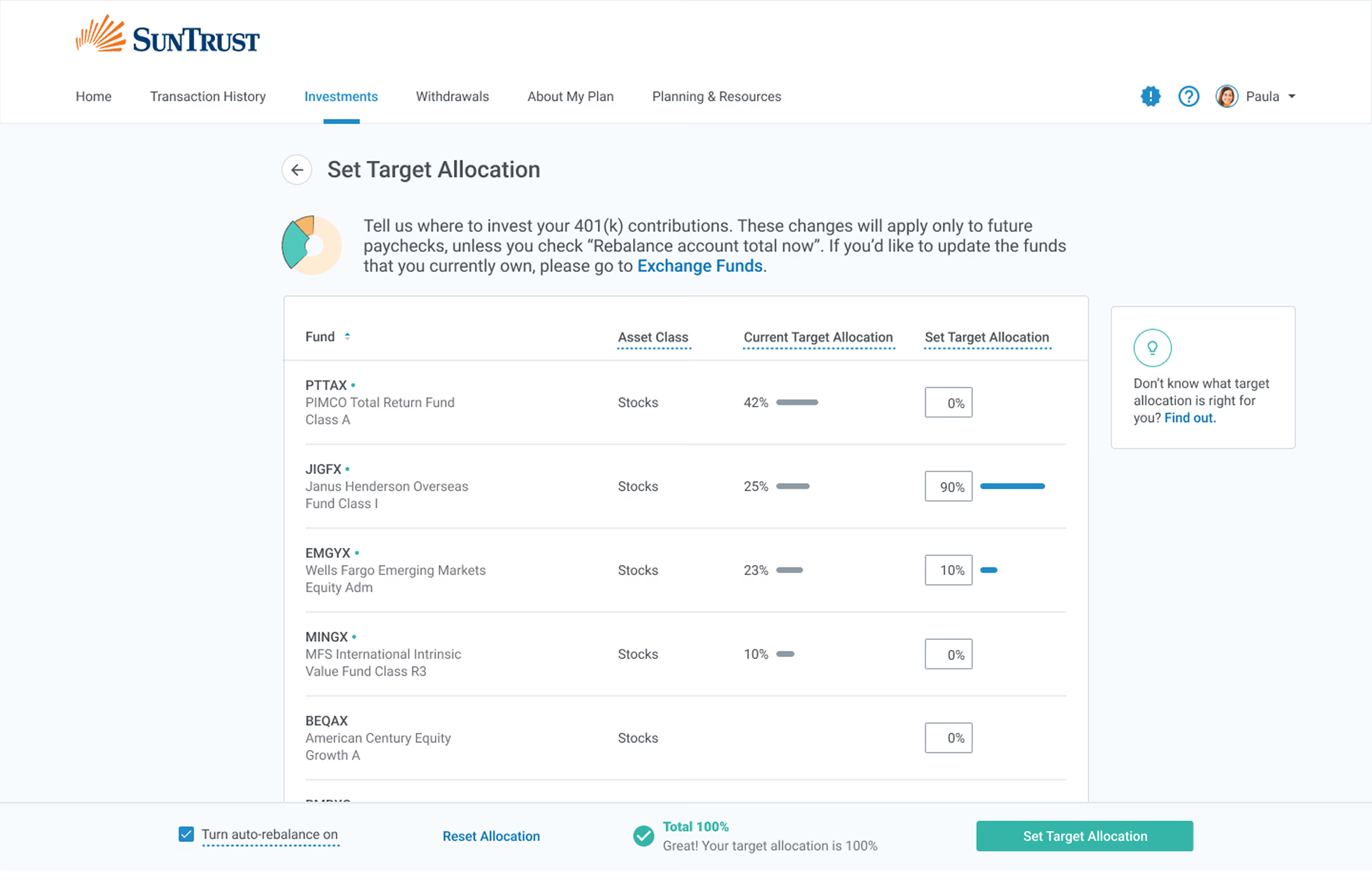

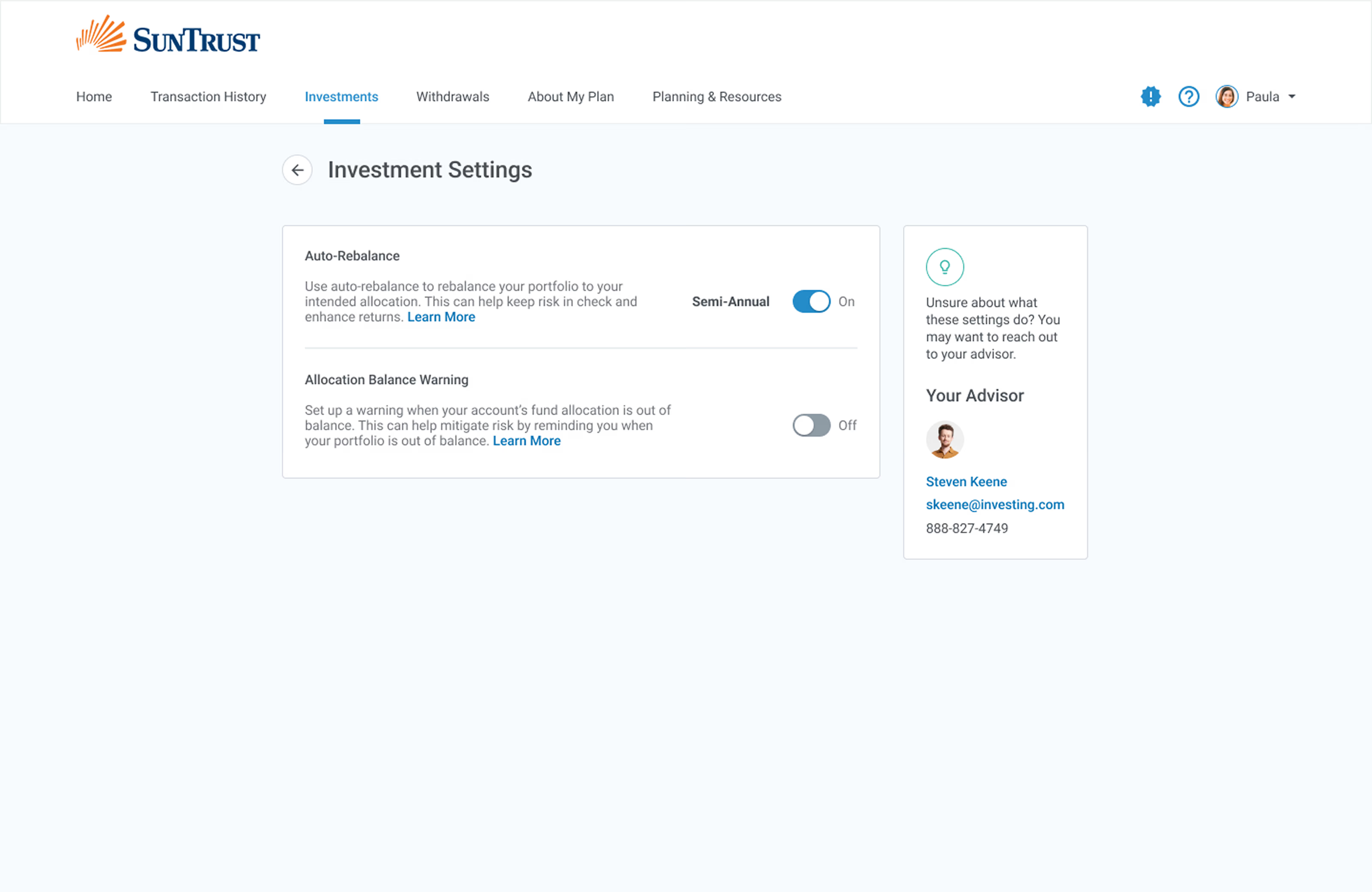

I rebuilt the IA around three levels, each tied to an intent rather than a data category. Home held the top-level jobs — transactions, investments, withdrawals, plan info, resources. Investments became the core management surface: balances, my funds, all funds, education, support. And the high-consequence actions — fund details, settings, target allocation, rebalance, fund exchange — got pulled into a level of their own.

The decision that mattered: separating viewing investments from acting on them. The old interface collapsed the two together, which fed both the error rate and the sense of overwhelm. Giving the consequential actions their own level meant people could review before they committed, instead of correcting after.

TESTING & THE HI-FI

Six people, eight tasks, one flow that told me where to dig.

I tested the low-fi prototype with six participants spanning the experience spectrum, on eight tasks across the full management workflow. Core navigation and fund discovery hit ceiling — 100% success, no errors. Exchanging investments was the only task that came in under, at 85%, so that’s exactly where the hi-fi attention went.

Testing also handed me three things I hadn’t scoped: splitting Roth and Regular balances apart, clearer step sequencing in the Set Investments flow, and CSV/XLS export for the power users. All three made it into the build.

Two decisions carried most of the weight in the hi-fi. The first was the one the IA had been pointing at all along — keeping viewing and acting apart, so the landing page leads with management actions and the dangerous flows live somewhere you have to go on purpose.

The second was making system state legible at every step: the running total in target allocation, the confirmation in fund exchange, the live sell value during a rebalance. In a product where one wrong move has real consequences, showing people what’s about to happen before they commit isn’t polish — it’s trust. Testing backed it up: the flows with the strongest real-time feedback scored highest on ease of use.

“I want to be able to dig into my investments more.”

WHAT HAPPENED

One month in, every number moved the right way.

The figures below come from one month of post-launch data against a three-month pre-launch benchmark. It’s directional — a month isn’t a verdict, and I’d say so in the room — but all four moved together, which is about as clean a signal as you get this early.

−60%

error rate during investment management tasks.

−29%

inbound support requests.

+25%

user satisfaction, from in-product surveys.

+21%

use of the embedded financial literacy tools.

THE SHIPPED EXPERIENCE /

WHAT I'D KEEP, WHAT I'D CHANGE

Two things this one taught me.

WHAT I'D KEEP

Recruit for the range, not the median.

Designing for the first-timer and the monthly-auditing accountant in the same product forced structural calls a single-persona approach would have skated right past — most of all the decision to isolate the high-consequence actions. The diverse recruit wasn't just methodologically tidy; it's what shaped the IA.

WHAT I'D CHANGE

Hold the measurement on a longer leash.

The honest limit here is the window. One month against a three-month benchmark told me the direction was right, but I'd have wanted a second and third month before treating any of these numbers as settled. Next time I'd build the longer read into the plan from the start, instead of letting launch feel like the finish line.

NEXT CASE STUDY — 001

Districts were renewing $1.5M in app licenses on gut feel.